Business & Tech

Make Sure You're Covered Before You Meet Irene

A few suggestions about what kinds of insurance policies you may need.

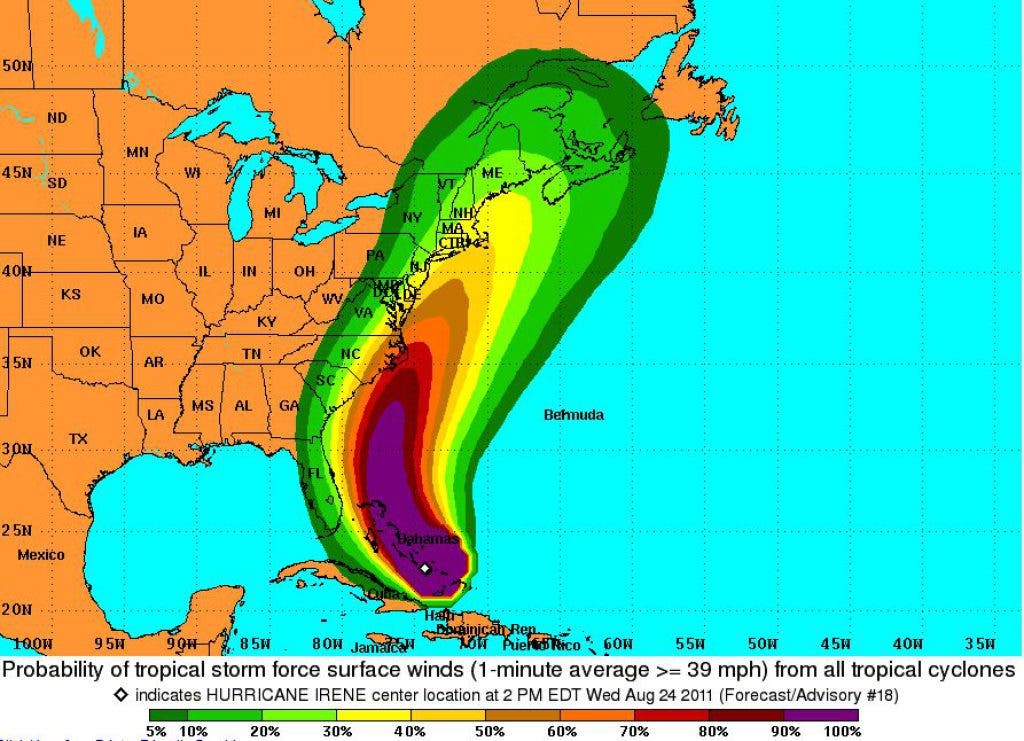

With the winds of Hurricane Irene aiming this way, one thing homeowners should also be thinking about is whether they can afford to pay for any damage done to their property.

Because the day after a hurricane is too late to find out you’re not covered, The Hartford insurance company has offered a few suggestions to consider now. Check these things out with your own insurance agent.

Lisa Lobo, consumer insurance expert for The Hartford, recommends looking at the following eight items to make sure you have the proper coverage:

1. Wind Coverage: “Many homeowners aren’t aware of the need for wind coverage or if they have wind coverage,” says Lobo. In the event of a hurricane, you must have wind coverage within your home insurance policy to receive compensation for damage. If you live in a high risk coastal area, you may need to purchase wind coverage from your state wind pool or association, or from a surplus lines insurer.

2. Flood insurance: Flood insurance is not covered on homeowners policies – it is a separate insurance policy that is needed to cover damage that results from flooding, even if the flooding was caused by a hurricane. For more information on flood insurance, visit the Federal Emergency Management Agency’s information page at www.fema.gov/nfip .

3. Deductibles: You may have a different deductible for a storm than you would for an event like a burglary or fire. Your policy may have a hurricane deductible or a wind deductible. These deductibles are typically based on a home’s insured value and are a percentage of your home’s value at the time of the storm, rather than the traditional set dollar deductible. If, for example, a house is insured for $100,000 and has a 2 percent deductible, the first $2,000 of a claim would be paid by the policyholder. Percentage deductibles may vary from 1 to 5 percent. And in some coastal areas with high wind risk, wind or hurricane deductibles can be even higher.

4. Students: If you have a child living away from home while in school, you may be eligible to receive compensation for your child’s items that may have been damaged during a storm at his or her school. Check with your insurance agent or insurance carrier to see what might be covered.

5. Reimbursement for living expenses: Most policies include reimbursement for living expenses if you are forced to live elsewhere while storm damage to your home is repaired, but this does not include lodging costs if you are simply forced to evacuate your home. Planning for these expenses ahead of time can make evacuation go more smoothly.

6. Replacement costs: Check to see if your policy will cover the replacement cost of your property or only its actual cash value (ACV), which factors in depreciation. It’s not uncommon for policies to provide actual cash value for damaged possessions. For example, you may only be reimbursed $500 for the $2,000 television purchased a few years ago. Another item to keep in mind is that a standard policy generally requires the homeowner to carry a limit that is at least 80 percent of the current cost to rebuild the home. Whichever type of policy you have, it’s a good idea to make your insurance company aware of any recent upgrades and ensure that you have adequate coverage when you need it.

7. Auto coverage: Check your auto policy to see what might be covered if your vehicle is damaged in a storm. Most comprehensive policies cover storm-related damage, including flooding. So it’s best to check with your agent or insurance carrier directly to ensure you have the right protection in place.

8. Storm-resistant improvement credits: Ask your insurance provider if you are eligible for credits for hurricane-resistant improvements, such as storm shutters. You might be able to save some money.

Facing a natural disaster is a challenging experience, but having the proper insurance protection in place will help ensure things return to normal as soon as possible if a storm strikes your property. If you would like more information on how to get prepared or file a claim after a storm, The Hartford has resources available at www.thehartford.com/heretohelp.

Get more local news delivered straight to your inbox. Sign up for free Patch newsletters and alerts.